The just-released 2019 Survey of Consumer Finances (SCF) from the U.S. Federal Reserve highlights massive and long-standing disparities in wealth in the United States — both between racial and ethnic groups, as well as within them.

The survey finds the typical White family in America has eight times the wealth (defined as gross assets minus liabilities) of the typical Black family, and five times the wealth of the typical Hispanic family:

- White families have the highest level of both median and average family wealth: $188,200 and $983,400, respectively.

- Black families’ median and average wealth is less than 15 percent that of White families, at $24,100 and $142,500, respectively.

- Hispanic families’ median and average wealth is less than 20 percent that of White families, at $36,100 and $165,500, respectively.

Other families—a diverse group that includes those identifying as Asian, American Indian, Alaska Native, Native Hawaiian, Pacific Islander, other race, and all respondents reporting more than one racial identification—have lower wealth than White families but higher wealth than Black and Hispanic families.

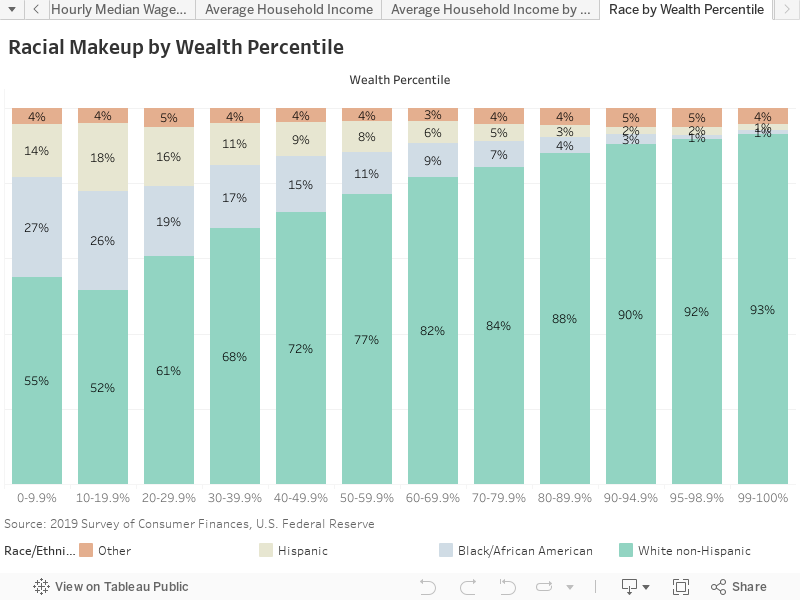

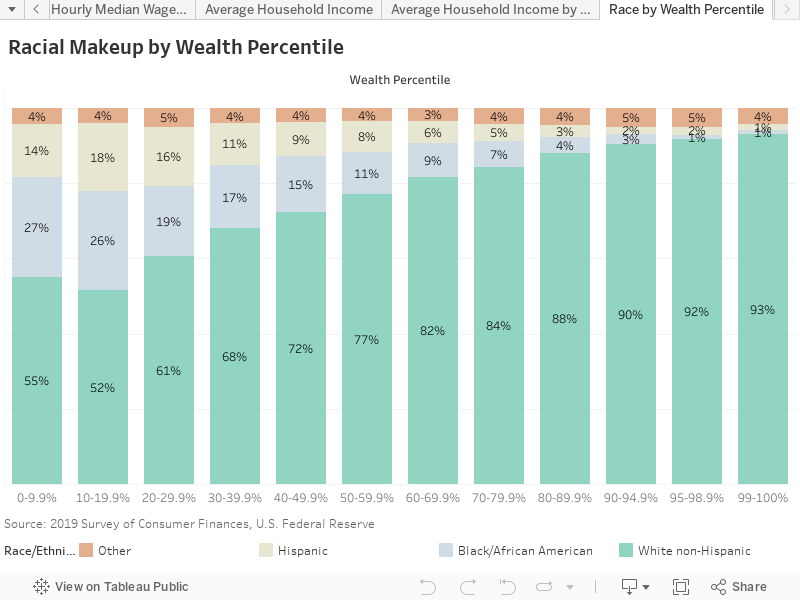

More Wealth = More Likely to be White

Pick a person at random in America and the more wealthy they are, the more likely it is they are White. By comparison, the bottom half of society is far more racially diverse.

Wealth is Highly Unequal Within Racial Groups

The overall differences between racial groups are not the only significant finding in the 2019 survey. There is also very significant wealth inequality within racial groups, as Matt Breunig’s analysis at the People’s Policy Institute notes:

“In every racial group, the top 20 percent of families owns around 85 percent of the racial group’s wealth, while the bottom half of families own less than 3 percent.”

Lessons from the Great Recession — and Solutions for a Different Future

Since the 2019 SCF was conducted largely before the onset of the COVID-19 pandemic, it doesn’t reflect how these groups are faring economically today – but if data from previous surveys is any indication, the results are not promising. According to the Fed:

“Median wealth fell about 30 percent for all groups during the Great Recession. However, Black and Hispanic families’ wealth continued to fall an additional 20 percent from 2010 to 2013, while White families’ wealth was essentially unchanged, and other families’ wealth fell a more modest 10 percent.

After 2013, median wealth rose for all groups, with faster growth for Black, Hispanic, and other families. [But] despite growth over the last two surveys, the typical White family and the typical Black family have yet to recover to their pre-Great Recession levels of wealth.”

Wealth inequality is driven by many sources — including the erosion of worker bargaining power, gender- and race-based pay discrimination — but one thing underpins them all: public policy.

Our economy is the way it is because of the policy choices of the past. While there’s no single panacea, there are a host of policy choices we can make today that will reshape our future for the better, including:

- Improving worker bargaining power: The Century Foundation highlights nine strategies to build impact and value for the modern labor movement in advocacy, benefits provision and administration, worker training and supply, worker ownership and more.

- Closing the gender pay gap: The Center for American Progress lists seven actions that can shrink the gender pay gap, including: minimum wage (and tipped minimum wage, for states that have one) increases, fair scheduling and pay transparency laws, and investments in high-quality childcare and early childhood education.

- Bridging the racial wealth divide: The Institute for Policy Studies offers ten solutions designed to strike at the structural underpinnings holding the racial wealth divide in place. Among them: baby bonds, Medicare for all, postal banking, and tax increases on the ultra-wealthy.

With election season upon us, there’s no better time to be in touch with your federal, state and local candidates for public office!

More To Read

State of Working Washington

August 10, 2021

New State Programs May Ease a Short-Term Evictions Crisis, but Steep Rent Hikes Spell Trouble

State and local lawmakers must fashion new policies to reshape our housing market

State of Working Washington

November 20, 2020

We Can Invest in Us

Progressive Revenue to Advance Racial Equity

Stacey Jones

Great to see EOI keeping the focus on this issue! Measures like that EOI has advocated for in the past–the Unearned Income Tax and the Estate Tax–as well as simply a wealth tax, would help here as well. So would a progressive income tax. A stronger safety net (wealth serves as a safety net) and fairer access to higher education (access that depends less on wealth) would help too! So much work to do here- important work.

Oct 3 2020 at 11:36 AM